The Hidden Costs of Credit Card Processing: A Merchant's Breakdown

The Hidden Costs of Credit Card Processing: A Merchant's Breakdown

Unpacking the Basics of Credit Card Fees

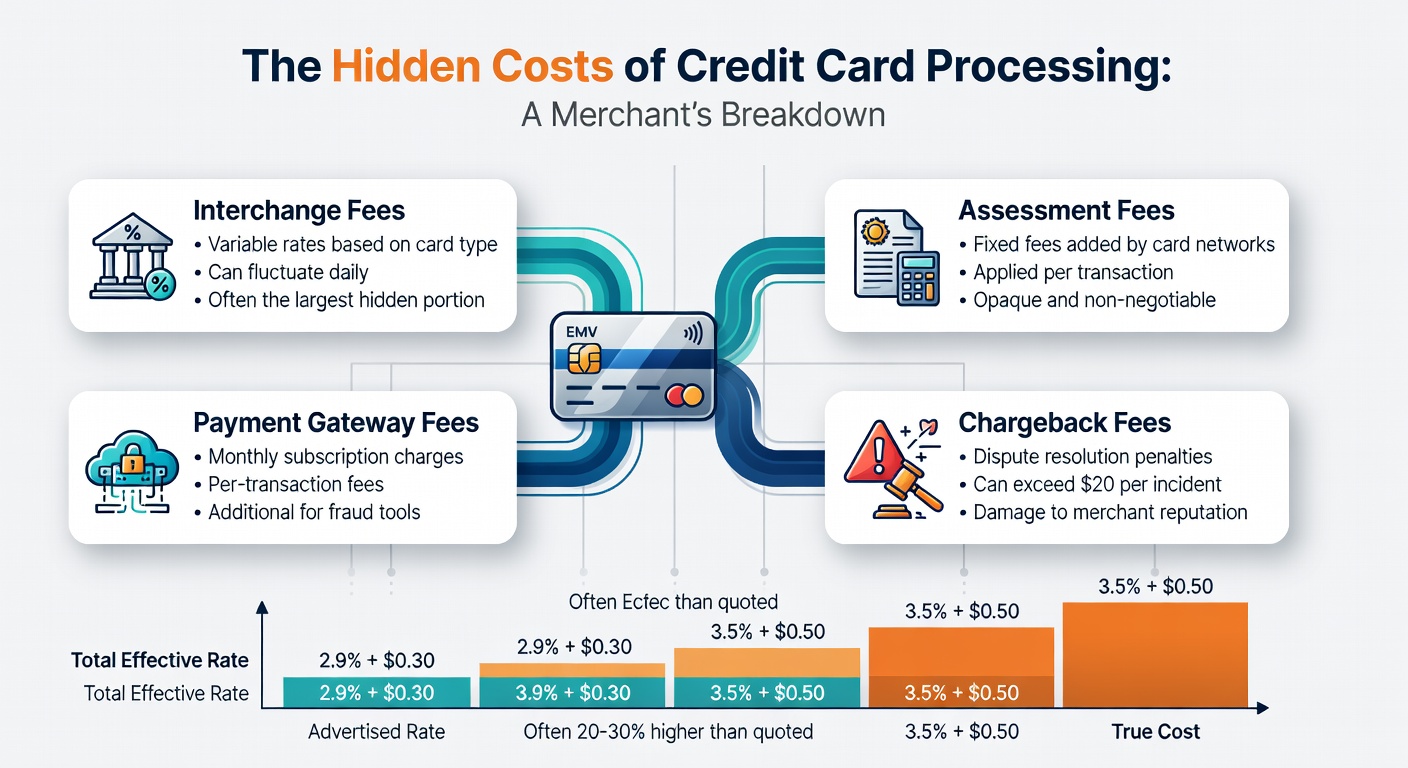

Merchants dive into credit card processing expecting straightforward transactions, yet layers of fees emerge that add up quickly; interchange fees, the largest chunk paid to card-issuing banks, often range from 1.5% to 3.5% per swipe, while assessment fees from networks like Visa and Mastercard tack on another 0.13% to 0.15%, and that's before processors layer in their markups. Data from the Nilson Report reveals that global merchants shelled out $48.6 billion in interchange fees alone in 2023, a figure projected to climb as card usage surges. Small businesses, handling thousands of transactions monthly, watch these percentages erode slim margins, especially since rates fluctuate based on card type—rewards cards hit harder at 2.5% or more, whereas debit cards hover lower around 0.5%.

But here's the thing: those headline rates merchants negotiate? They rarely tell the full story, because tiered pricing structures—qualified, mid-qualified, non-qualified—shift costs based on how transactions code, with non-qualified swipes jumping fees by 1% or higher if equipment lags or customers use foreign cards. Observers note how one retailer, processing $500,000 annually, faced an extra $10,000 yearly from mid-qualified tiers alone, a surprise uncovered only after dissecting statements.

Chargebacks: The Silent Profit Killer

Chargebacks strike when customers dispute transactions, forcing merchants to refund plus absorb the original fee—typically 1% to 2% of sales volume annually, according to Federal Reserve studies—and disputes have spiked 20% since 2020 amid rising e-commerce fraud. Networks rule 65-80% in favor of cardholders, leaving merchants out $25 billion globally each year; resolution demands time too, with representment fees hitting $15 to $100 per case, and failed disputes trigger velocity limits that throttle future processing.

Take one coffee shop chain where friendly fraud—legit charges reversed for perks—accounted for 40% of disputes; owners scrambled with prevention tools costing $500 monthly, yet losses persisted. And while programs like Visa's Visa Claims Resolution promise faster rulings by April 2026, early pilots show mixed results, with merchants bracing for adjusted liability shares under evolving rules.

PCI Compliance: More Than Just a Checkbox

PCI DSS compliance looms large, mandating secure handling of card data, yet non-compliance penalties from processors reach $5,000 to $100,000 monthly; merchants undergo scans quarterly, with self-assessment questionnaires for smaller outfits but full audits for high-volume ones exceeding $3 million in processing. Research from the PCI Security Standards Council—wait, actually drawing from Verizon's annual reports—indicates 83% of breaches tie to third-party vulnerabilities, pushing merchants toward certified gateways at $20 to $200 monthly, plus encryption upgrades running thousands upfront.

Those who've skimped discover fines compound fast; a mid-sized retailer paid $21,000 in 2024 after a lapse, while ongoing training for staff adds $50 per employee yearly. Semicolons link this to hardware mandates too, since outdated terminals fail scans, triggering surcharges.

Equipment, Terminals, and Software Sneak-Ins

Leasing terminals sounds simple at $20-50 monthly, but early termination fees claw back $500 or more, and proprietary software locks merchants into ecosystems where upgrades cost $300 apiece; mobile setups promise flexibility yet demand $99 reader fees plus 2.9% + $0.30 per tap. Batch fees—$0.25 per closeout—pile up for daily settlers, while inactivity charges ding dormant accounts $10-25 monthly, a trap for seasonal sellers.

What's interesting here: integrated POS systems bundle processing but embed markups merchants overlook, like one boutique uncovering $2,000 annual gateway fees hidden in "platform access." And now, contactless mandates accelerate costs, with EMV upgrades averaging $5,000 for chains.

Reserves, Rolling Reserves, and Cash Flow Hits

Processors hold 5-10% of monthly volume in reserves for 6-12 months, citing risk, which freezes capital—critical for inventory-heavy merchants facing 30-day terms from suppliers. High-risk categories like CBD sales see 20% holds, turning $100,000 sales into $20,000 locked funds; truth-in-processing mandates require disclosure, yet vague terms allow extensions.

Experts observe how one importer lost $15,000 in held reserves during a supply crunch, scrambling for bridges while fees accrued on borrowed capital. That said, April 2026 brings scrutiny from the Consumer Financial Protection Bureau updates, potentially capping reserves for standard-risk merchants under fair lending probes.

Monthly Fees and the Fine Print Trap

Statement fees ($10-25), PCI reports ($50-150), AVS gateway access ($15), even paper statements at $1 each accumulate; gateways charge setup $100 plus annuals $120, and multi-MID setups for omnichannel multiply them. Data indicates small merchants forfeit 0.5% extra revenue to these fixed costs, eroding 20% of net profits on $1 million volume.

People often find quarterly minimums—$25 enforced—bite hardest during slow seasons, forcing unprofitable swipes just to meet them. Semicolons connect this to termination clauses too, where 90-day notices plus PCI residuals linger years post-cancel.

The Toll on Small and Mid-Sized Merchants

Figures from Payments Canada show SMBs pay 25% higher effective rates than enterprises due to volume tiers, with U.S. merchants averaging 2.7% blended costs versus 1.9% for giants; Australian merchants face similar squeezes, per Reserve Bank data, where surcharging caps limit pass-throughs. One study tracked a franchise losing $18,000 yearly to unoptimized processing, margins shrinking from 8% to 4%.

Yet trends shift: surcharging legality expands in the EU under 2026 PSD3 rules, allowing fee recovery, although compliance audits loom. Observers track how tokenization cuts disputes 30%, but adoption lags at 40% for independents.

Navigating Trends Through 2026 and Beyond

Real-time payments challenge cards, yet processing clings with buy-now-pay-later integrations hiking interchange 1-2%; AI fraud tools promise savings—Verizon reports 25% chargeback drops—but setup runs $1,000-5,000. April 2026 marks pivotal shifts too, as U.S. Durbin Amendment expansions cap debit fees further, and EU caps tighten to 0.2% for credit, per European Commission proposals, reshaping merchant math.

Those monitoring see networks pushing volume-based incentives, yet independents gain leverage negotiating pass-through pricing—pure interchange without markup bloat.

Conclusion

Hidden costs in credit card processing weave through fees, disputes, compliance, and holds, collectively devouring 3-5% of revenue for many merchants; dissecting statements quarterly uncovers leaks, while volume benchmarks and gateway switches reclaim thousands. As regulations evolve toward April 2026, data underscores adaptation's edge—merchants who audit processors save 20-40% on effective rates, turning burdens into balanced operations. The landscape demands vigilance, but facts equip those ready to break it down.