Navigating Chargeback Patterns in Recurring Mobile Commerce Through Adaptive Processing Frameworks

Chargeback patterns in recurring mobile commerce have shifted noticeably in recent years, with merchants facing elevated dispute rates tied to subscription services, in-app purchases, and digital content renewals. These transactions often repeat on fixed cycles, which creates predictable windows where cardholders may dispute charges due to forgotten enrollments, service dissatisfaction, or unauthorized use. Industry data compiled through 2025 shows that mobile recurring billing accounts for a growing share of overall chargeback volume, particularly in regions where smartphone penetration exceeds 85 percent of the adult population.

Identifying Recurring Chargeback Patterns

Observers tracking payment ecosystems note distinct clusters in dispute reasons that surface most often in mobile subscriptions. Friendly fraud, where legitimate cardholders claim they never authorized a recurring charge, represents one of the largest categories, while unrecognized merchant descriptors and failed cancellation attempts form additional clusters. Research from payment network analyses indicates that disputes peak between day 25 and day 35 of a billing cycle in many markets, coinciding with statement arrival dates. Geographic variations appear as well; North American markets show higher rates of post-renewal disputes, whereas European users more frequently cite billing descriptor confusion according to aggregated processor reports.

Patterns also correlate with specific verticals. Streaming services and fitness apps experience elevated chargeback ratios during promotional trial conversions, while gaming platforms report spikes after seasonal content drops. These trends have prompted processors to refine monitoring tools that flag accounts showing velocity changes or descriptor mismatches before the next billing event occurs.

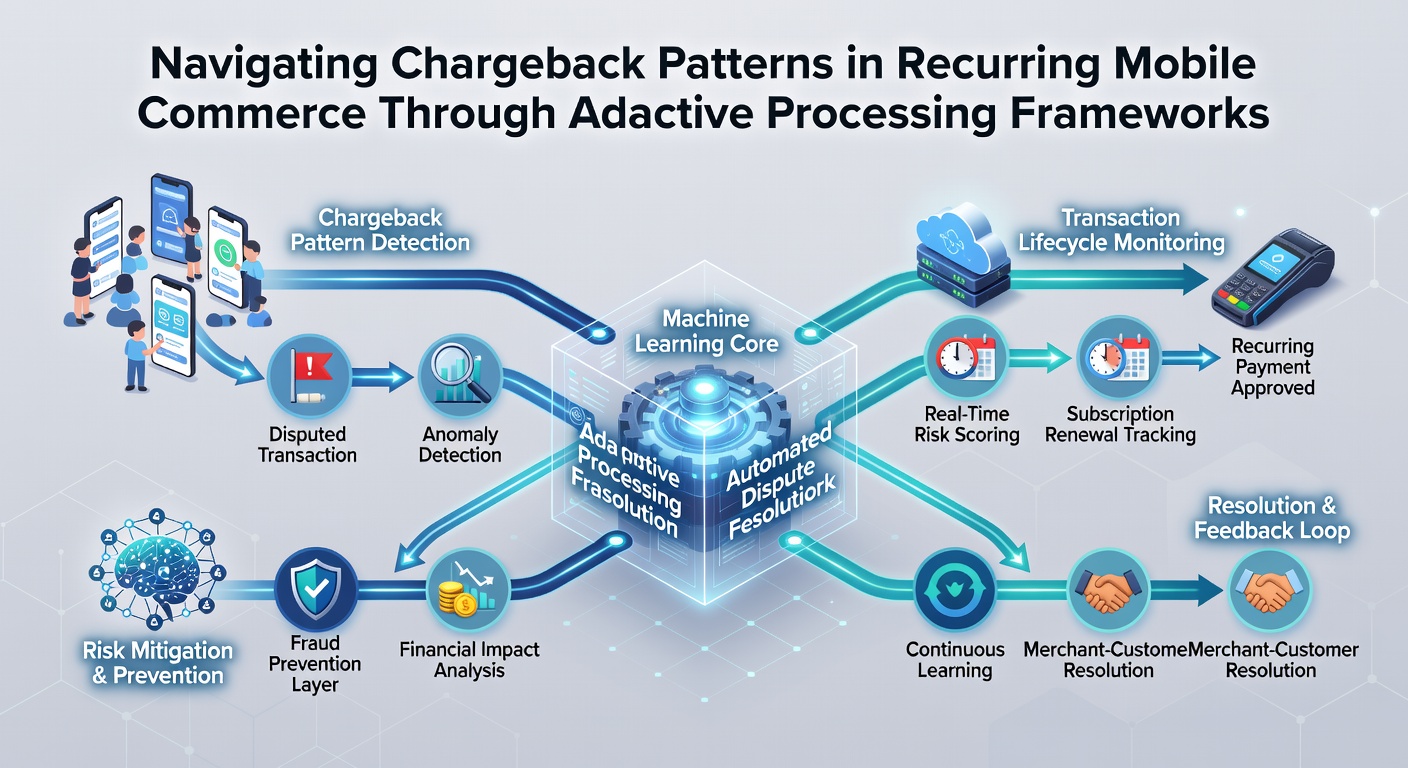

Adaptive Processing Frameworks in Action

Adaptive processing frameworks apply machine learning models that adjust authorization rules in real time based on historical dispute data and transaction context. Rather than relying on static velocity checks or fixed amount thresholds, these systems recalibrate risk scores for each recurring transaction using signals such as device fingerprint consistency, prior billing success rates, and regional dispute propensity. When a pattern emerges, for example, a cluster of disputes linked to a particular descriptor length, the framework can automatically trigger descriptor updates or insert confirmation steps for affected subscribers.

Implementation typically begins with integration of transaction-level data feeds into centralized decision engines. These engines then apply multi-layered scoring that weighs both issuer-side data and merchant-specific history. In practice, frameworks deployed by large mobile commerce platforms have demonstrated the capacity to reduce chargeback ratios by rerouting high-risk renewals through additional verification layers without broadly impacting approval rates. The approach differs from earlier rule-based systems because parameters evolve continuously as new dispute data enters the model.

Data Sources and Regulatory Context

According to figures released by the Federal Trade Commission, consumer complaints involving recurring mobile charges increased steadily through early 2026, prompting closer scrutiny of billing practices. In parallel, European Central Bank statistical releases from the same period highlight similar upward movement in cross-border mobile disputes within the Single Euro Payments Area. Merchants operating across these jurisdictions have therefore adopted frameworks that incorporate jurisdiction-specific compliance checkpoints while maintaining unified processing logic.

One study conducted by academic researchers at the University of Melbourne examined 18 months of anonymized mobile billing records and found that adaptive scoring reduced dispute incidence most effectively when models incorporated at least six prior billing cycles of data per subscriber. The findings underscored the value of longitudinal signals over single-transaction attributes.

Operational Considerations for Merchants

Merchants integrating these frameworks typically begin by mapping their current chargeback root causes against available data fields. This mapping exercise reveals whether descriptor standardization, pre-renewal notifications, or step-up authentication would yield the greatest impact. Once priorities are set, teh framework receives configuration parameters that align with those findings, after which performance is tracked through weekly dispute ratio dashboards.

Teams responsible for ongoing management monitor model drift, adjusting weights when new dispute typologies surface. In May 2026, several processors introduced enhanced descriptor validation modules that cross-reference billing text against known complaint triggers, providing an additional layer within the adaptive stack. These updates arrived alongside revised network rules that placed stricter liability allocation on merchants failing to maintain clear recurring billing disclosures.

Conclusion

Chargeback navigation in recurring mobile commerce now centers on frameworks capable of continuous recalibration rather than fixed defenses. As transaction volumes grow and regulatory expectations tighten, the systems that ingest fresh dispute data and adjust authorization logic accordingly have become central to maintaining stable acceptance rates. Merchants who align their operational data flows with these adaptive capabilities position themselves to respond directly to emerging patterns without disrupting legitimate subscriber activity.