13 Jun 2026

Merchant Accounts Meet Mobile APIs: Strategies for Reducing Cross-Border Fraud Incidents

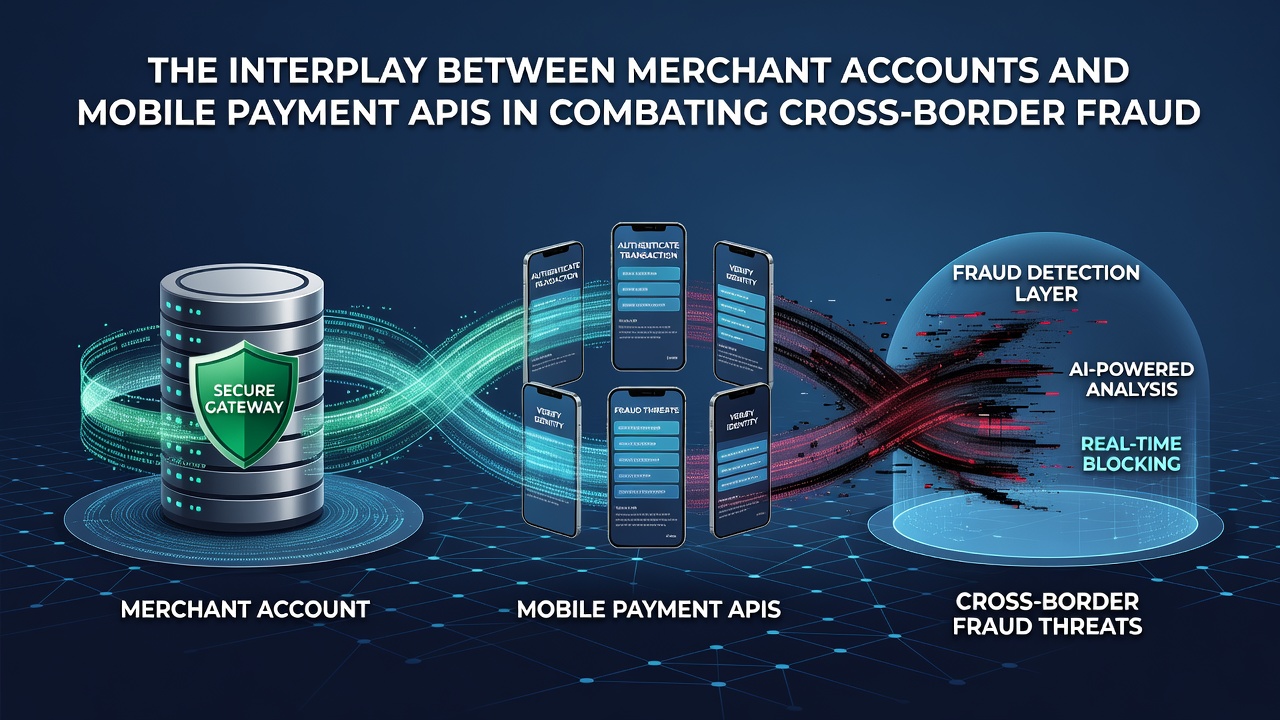

Merchant accounts serve as the foundational banking relationships that allow businesses to accept payments, while mobile payment APIs provide the technical bridges that process those transactions in real time across devices and regions. When these two elements work together they create layered defenses against cross-border fraud, which involves unauthorized transactions that cross national boundaries and exploit differences in regulatory environments, currency systems, and verification standards.

Core Functions of Merchant Accounts in International Settings

Merchant accounts handle settlement, risk assessment, and compliance checks that vary by country, and they maintain records that help identify patterns in high-risk regions. Banks and processors review application details including business history, expected transaction volumes, and geographic focus before approving these accounts, then they apply ongoing monitoring to flag unusual activity such as sudden spikes in international volume or mismatched billing addresses. Research from payment networks shows that accounts with robust underwriting reduce chargeback rates by verifying merchant legitimacy upfront rather than reacting after losses occur.

Mobile Payment APIs as Real-Time Gatekeepers

Mobile payment APIs manage authentication flows, token generation, and device fingerprinting that occur during each transaction attempt. These interfaces pull data from multiple sources including device location, IP address, and behavioral signals to score risk before authorization completes. In cross-border scenarios APIs often enforce additional steps such as two-factor confirmation or velocity checks that limit rapid successive purchases from the same account. Observers note that APIs can adapt rules dynamically based on the merchant account's risk profile, creating a feedback loop where historical data informs immediate decisions.

Integration Points That Strengthen Fraud Controls

The interplay begins during onboarding when a merchant account links to specific API endpoints that carry pre-set fraud parameters tailored to cross-border traffic. Once connected the system shares signals such as previous decline reasons or known compromised card data across both the account level and the API layer. This connection allows processors to apply geo-fencing rules that block transactions from certain high-risk corridors while permitting others based on merchant category. Data indicates that combined monitoring catches discrepancies faster than either component alone, because the merchant account supplies the business context that pure API analysis sometimes lacks.

Tokenization plays a central role here as well. APIs replace sensitive card details with tokens that merchant accounts store without exposing full numbers, which limits exposure if one side of the system faces a breach. In practice this means a transaction originating in one country can be validated against the merchant's established patterns in another without transmitting raw data repeatedly. Those who've studied these setups find that token reuse across borders requires explicit merchant account approval, adding an extra authorization gate.

Regulatory and Industry Data Shaping Current Practices

Figures from the European Central Bank reveal that cross-border card fraud accounted for a measurable portion of total payment losses in recent reporting periods, prompting updates to API security requirements that merchant accounts must implement. In parallel, reports issued by the Reserve Bank of Australia highlight how real-time API monitoring combined with merchant-level velocity limits has lowered unauthorized transaction rates in tested corridors. These developments illustrate how account-level policies and API capabilities reinforce each other under evolving compliance frameworks.

By June 2026 several payment processors plan to roll out enhanced API versions that incorporate machine learning models trained on aggregated merchant account histories. The models aim to predict fraud likelihood for specific origin-destination pairs, allowing accounts to adjust approval thresholds automatically. This approach builds on existing structures rather than replacing them, so merchants continue using familiar settlement processes while gaining stronger preventive tools.

Practical Mechanisms in Daily Operations

One common mechanism involves shared blacklists where a merchant account flags a card after repeated declines and the connected API blocks that card on subsequent attempts regardless of device or location. Another uses dynamic currency conversion controls that APIs enforce only when the merchant account has pre-approved the feature, preventing fraudsters from exploiting conversion gaps. Case examples from industry reports show that businesses operating in multiple regions achieve lower loss ratios when they align their account risk settings directly with API rule sets instead of managing them separately.

Device binding offers yet another layer. APIs tie tokens to specific mobile devices registered through the merchant account portal, which makes it harder for stolen credentials to succeed on new hardware. When a transaction arrives from an unrecognized device the system can require additional verification that the merchant account administrator has configured in advance.

Conclusion

Merchant accounts and mobile payment APIs together form a coordinated system that addresses the unique challenges of cross-border fraud through shared data, real-time checks, and adaptive rules. The technical connections between them allow each component to leverage the strengths of the other, resulting in faster detection and fewer successful unauthorized transactions. Continued alignment between account policies and API capabilities will determine how effectively the payments industry manages these risks as transaction volumes and international connectivity continue to grow.