Mechanics Behind Protected Subscription Payments: APIs, Merchant Setup, and Mobile Fraud Barriers

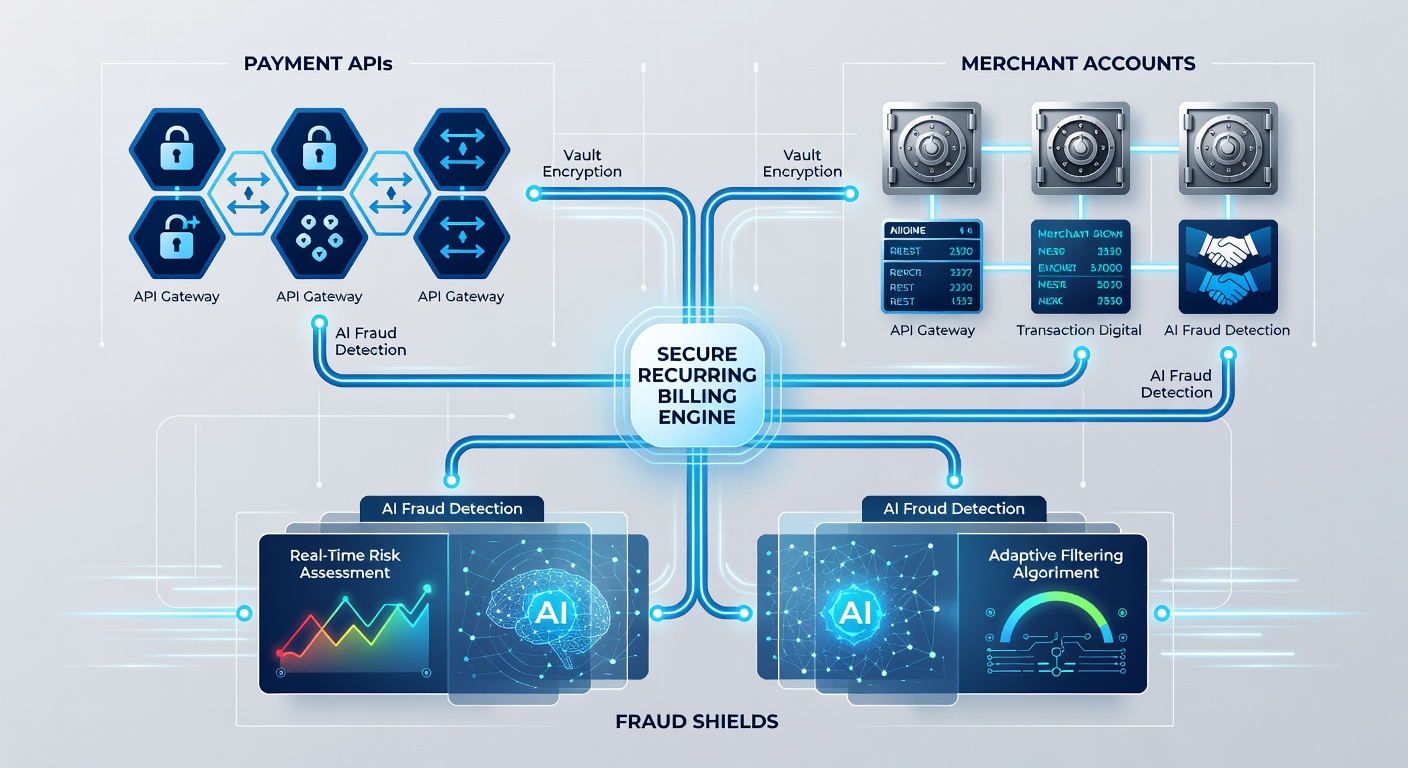

Payment APIs form the core connection point between mobile applications and financial networks, allowing developers to schedule and process recurring charges without storing sensitive card data on user devices. These interfaces handle token exchanges, authorization requests, and settlement cycles while meeting encryption standards set by international card networks. In practice, an API call initiates a subscription, returns a unique token for future billing, and triggers automatic pulls on the agreed schedule. Merchant accounts serve as the settlement layer that receives funds after each successful authorization. Providers open these accounts after verifying business legitimacy, reviewing transaction history, and confirming compliance with data-security protocols. Once active, the account routes approved payments through acquiring banks and distributes net amounts to the merchant after deducting interchange fees and processing charges.

Payment APIs form the core connection point between mobile applications and financial networks, allowing developers to schedule and process recurring charges without storing sensitive card data on user devices. These interfaces handle token exchanges, authorization requests, and settlement cycles while meeting encryption standards set by international card networks. In practice, an API call initiates a subscription, returns a unique token for future billing, and triggers automatic pulls on the agreed schedule. Merchant accounts serve as the settlement layer that receives funds after each successful authorization. Providers open these accounts after verifying business legitimacy, reviewing transaction history, and confirming compliance with data-security protocols. Once active, the account routes approved payments through acquiring banks and distributes net amounts to the merchant after deducting interchange fees and processing charges.API Integration Patterns for Recurring Charges

Developers embed API libraries directly into mobile codebases, then configure webhook endpoints that receive real-time updates on payment success, failure, or disputes. The setup supports multiple currencies and regions because leading gateways maintain connections to local banking rails. When a user subscribes, the initial call captures consent and creates a stored credential that subsequent charges reference automatically.

Research from payment-security councils shows tokenization reduces exposure during these handoffs because actual card numbers never travel to the merchant server after the first transaction. Instead, the gateway returns a network-specific token that works only for that merchant and device combination.

Merchant Account Requirements and Settlement Flow

Opening a merchant account involves submitting incorporation documents, bank references, and projected volume estimates. Underwriters assess risk categories based on industry type and chargeback history before approving processing limits. Once live, funds from successful recurring payments move through the account on a rolling basis, typically settling in one to three business days depending on the acquiring bank and risk profile.

Observers note that mobile-first merchants often request higher velocity limits because subscription models generate predictable daily inflows. Account statements detail each batch, including fees broken down by interchange tier, assessment, and gateway markup.

Fraud Detection Layers Tailored for Mobile Users

Mobile fraud shields combine device fingerprinting, behavioral analytics, and velocity checks that run before each scheduled charge. Systems compare current session data against historical patterns for the same account holder, flagging anomalies such as sudden location changes or mismatched device identifiers. When risk scores exceed thresholds, the transaction routes to manual review or declines automatically.

According to data published by the U.S. Federal Trade Commission, mobile recurring billing fraud attempts often exploit stored credentials after account takeover. Shielding tools therefore require step-up authentication for high-value renewals or after detected SIM swaps. European regulators have similarly emphasized strong customer authentication rules that apply to subscription renewals exceeding certain thresholds.

Combined Workflow in May 2026 Environment

By May 2026, updated PCI DSS requirements will mandate enhanced logging for every recurring authorization, including the exact API version and token reference used. Merchants who upgraded their gateways ahead of the deadline report smoother compliance audits because automated reconciliation matches each charge to its originating consent record. Mobile applications now surface in-app notifications that list upcoming billing dates and allow one-tap cancellation, reducing involuntary churn while maintaining clear audit trails.

Industry reports indicate that integrated platforms link the merchant account dashboard directly to fraud consoles, so risk teams can pause an entire subscription series from a single screen when patterns suggest coordinated testing of stolen credentials. This linkage shortens response time from days to minutes.

Conclusion

Secure recurring billing rests on three coordinated elements: payment APIs that manage tokens and schedules, merchant accounts that handle settlement and reporting, and layered fraud tools that monitor mobile-specific signals. When these components connect through compliant infrastructure, merchants maintain steady revenue streams while users receive predictable charges protected against unauthorized use. Continued alignment with evolving security standards will determine how smoothly the system scales for the next generation of subscription services.