Global Subscription Payment Barriers and Specialized API Solutions for Cross-Border Credit Card Processing

Subscription services have expanded rapidly into international markets, yet companies encounter persistent obstacles when handling credit card transactions from customers in multiple countries. Currency fluctuations, regional banking rules, and elevated decline rates create friction that disrupts recurring billing cycles. Data from payment industry reports shows that cross-border transactions experience failure rates up to three times higher than domestic ones, primarily because of mismatched authorization protocols and local compliance requirements.

These challenges intensify when businesses scale subscription models across continents. A company offering streaming content might process payments from users in Europe, Asia, and Latin America on the same platform, but each region imposes distinct restrictions on card data storage, tax calculations, and fraud screening. Without tailored technical bridges, merchants face revenue leakage from repeated declines and customer churn triggered by payment interruptions.

Core Credit Card Processing Obstacles in Worldwide Recurring Models

International subscription platforms must navigate varying interchange fees that differ by country and card network. European issuers often apply higher rates for non-euro transactions, while some Asian markets enforce strict data localization laws that prohibit storing card details on foreign servers. Observers note these inconsistencies lead to authorization delays averaging several seconds longer than standard domestic processes, which compounds during peak renewal periods.

Fraud detection systems add another layer of complexity. Global models trigger more frequent false positives because algorithms trained on one market misinterpret legitimate patterns from another. Research indicates that subscription services lose approximately 1.8 percent of potential revenue to such blocks each quarter, with the figure rising in regions where card-not-present transactions dominate. Tokenization through niche integrations helps by replacing sensitive card numbers with region-specific tokens that satisfy local regulators without exposing full details across borders.

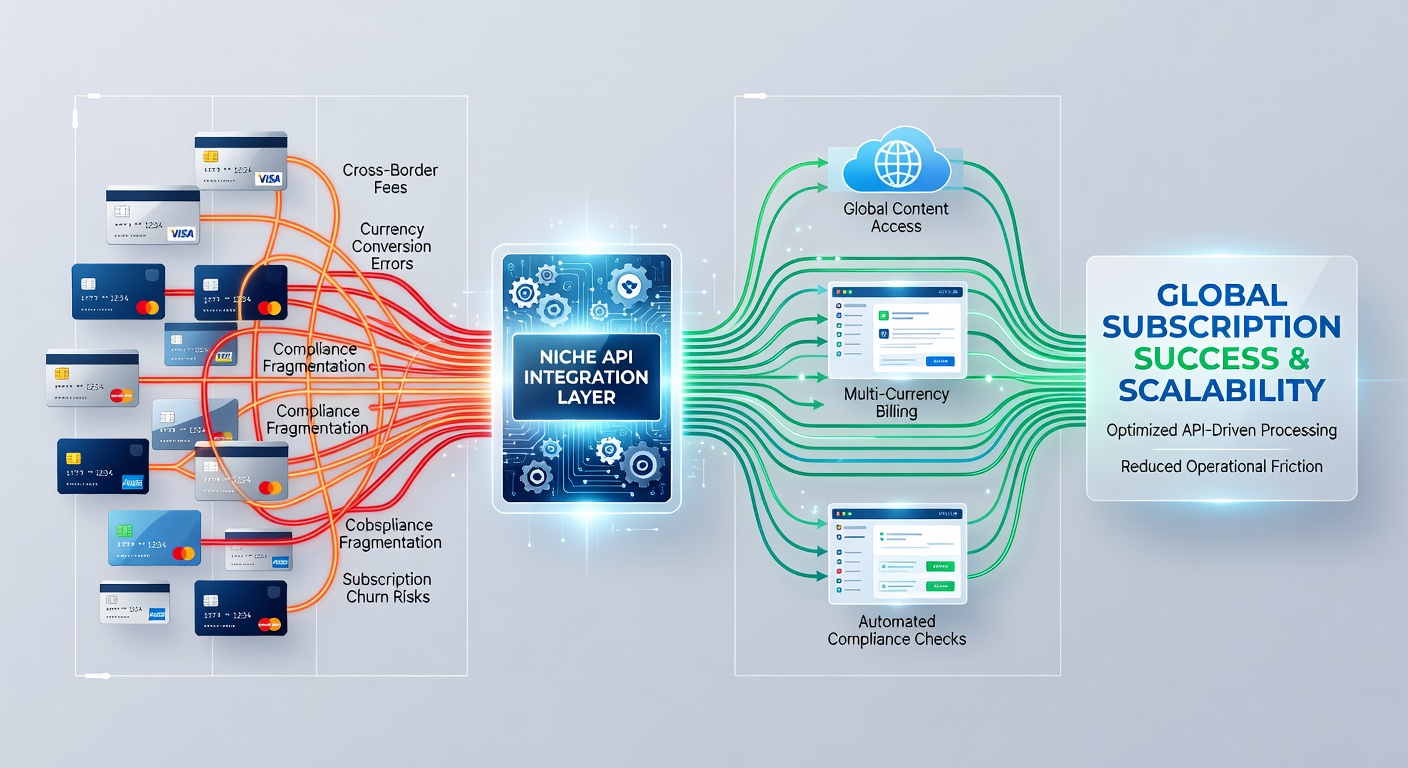

Targeted API Integrations as Practical Workarounds

Niche application programming interfaces connect subscription platforms directly to localized payment processors rather than relying on single global gateways. These specialized connections handle currency conversion in real time, apply country-specific fraud rules, and manage recurring billing schedules that align with local banking holidays. Companies that adopt such APIs report measurable reductions in decline rates, often by 25 to 40 percent within the first six months of implementation.

One integration approach involves embedding micro-services that communicate with domestic acquirers in each target market. For instance, a North American service expanding into Australia can route payments through an API that interfaces with the Reserve Bank of Australia's settlement systems, ensuring compliance with both PCI-DSS and local consumer protection statutes. This method avoids the broad-brush rules of major gateways that sometimes flag legitimate recurring charges as suspicious.

Implementation Patterns Observed in 2026

By May 2026, several subscription providers have layered multiple niche APIs to create hybrid processing stacks. These stacks automatically select the optimal route based on customer location, card type, and subscription tier. A basic plan might route through a low-cost European processor, while premium tiers use higher-security pathways in regulated markets such as Canada or Singapore. The flexibility stems from modular design that allows updates when new regulations emerge without rebuilding the entire system.

Integration teams focus on standardized webhooks that notify the subscription management software of authorization outcomes in under two seconds. This speed matters because customers expect immediate confirmation during sign-up or renewal. Data from industry analyses shows platforms using these targeted connections maintain retention rates 12 percent above those dependent on single-provider solutions.

Compliance and Security Considerations

Global subscription operators must satisfy overlapping regulatory frameworks including the European Union's payment services directives and equivalent standards in other jurisdictions. Niche APIs incorporate built-in compliance checks that adjust dynamically; for example, they enforce strong customer authentication requirements only where mandated rather than applying them universally. This selective approach reduces friction for users in regions without such mandates while maintaining security everywhere.

Encryption standards remain consistent across integrations, yet the actual key management occurs within each local processor's environment. Such distribution limits exposure if any single endpoint experiences a breach. Those who have studied payment security trends note that segmented architectures have become standard practice for services handling recurring international payments.

Conclusion

Subscription businesses operating across borders continue to refine their credit card processing through carefully selected API connections that address specific regional hurdles. These integrations streamline authorization, reduce decline incidents, and support compliance without sacrificing operational speed. As markets evolve, the ability to swap or add niche processors quickly provides a sustainable path for maintaining reliable recurring revenue streams worldwide.