Evolution of Secure Payment Processing: Merchant Accounts Leading to Advanced Mobile Billing Defenses

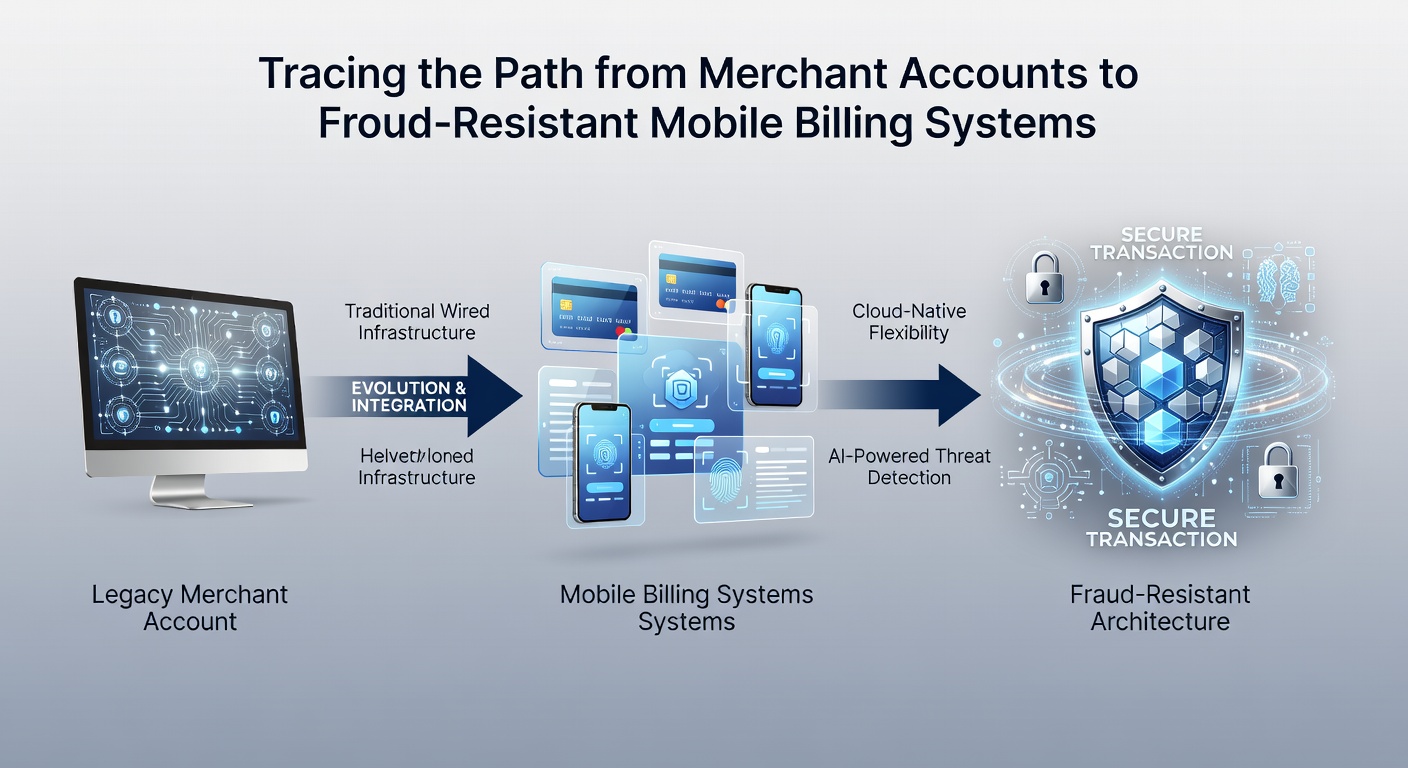

Merchant accounts emerged in the mid-20th century as businesses sought reliable methods to accept credit card payments, establishing direct relationships with acquiring banks that facilitated transaction processing and settlement into merchant bank accounts, while those accounts carried inherent risks including chargebacks and unauthorized use that grew alongside expanding card networks.

Traditional setups required merchants to undergo underwriting processes where banks evaluated business history, credit scores, and projected volumes before approving accounts, and once active those accounts handled authorizations through batch processing that often left windows for fraudulent activity to go undetected until reconciliation occurred days later.

Early Fraud Challenges in Merchant Account Operations

Data from regulatory bodies shows that chargeback rates climbed steadily through the 1990s and early 2000s as e-commerce expanded, prompting acquiring banks to implement basic verification steps such as address verification services and card security codes, although these measures addressed only surface-level issues while sophisticated schemes involving stolen card details continued to evolve.

Observers note that merchants operating high-risk categories faced elevated fees and reserves held against potential losses, creating financial pressures that encouraged exploration of alternative billing models, and those pressures intensified when recurring subscription services gained popularity because repeated billing cycles multiplied exposure points for fraudsters.

Transition Toward Digital Integration and Mobile Platforms

Mobile billing systems began gaining traction in the 2010s as smartphone adoption accelerated, allowing direct carrier billing and app-based payments that bypassed some traditional merchant account friction points, yet early versions still relied on underlying card data storage that exposed systems to breaches until tokenization techniques advanced.

Research indicates that by 2020 integration between merchant accounts and mobile gateways had accelerated through API connections that enabled real-time authorization without storing sensitive card numbers on merchant servers, and this shift reduced certain attack vectors while introducing new considerations around endpoint security on consumer devices.

According to reports from the European Banking Authority, cross-border mobile transactions in 2025 demonstrated measurable declines in fraud incidence when tokenization combined with device fingerprinting was deployed at scale, and similar patterns appear in data released by the Australian Payments Network showing adoption of these layered defenses correlating with lower dispute volumes for participating merchants.

Technological Layers Enabling Fraud Resistance

Tokenization replaces primary account numbers with unique tokens that hold no intrinsic value if intercepted, allowing mobile billing platforms to process recurring charges while limiting exposure, and when paired with behavioral analytics these tokens support continuous authentication that flags anomalies such as unusual locations or spending patterns in real time.

Artificial intelligence models trained on transaction histories now monitor mobile billing flows for indicators of account takeover or synthetic identity fraud, with systems updating thresholds dynamically as new patterns emerge, and financial institutions report that such monitoring operates alongside compliance frameworks established by bodies like the Bank of Canada to maintain standardized security expectations across regions.

Studies from academic sources including those published through university payment research centers reveal that merchants migrating from legacy account structures to integrated mobile billing often experience streamlined onboarding because digital platforms automate much of the verification previously handled through manual reviews, although legacy accounts continue serving businesses with specialized requirements that mobile options have not fully supplanted.

Current Landscape as of May 2026

As of May 2026, adoption metrics indicate that a majority of new mobile billing implementations incorporate multiple defensive layers including end-to-end encryption, biometric prompts on consumer devices, and machine learning classifiers that achieve high precision in distinguishing legitimate recurring payments from fraudulent attempts, and these implementations frequently connect back to original merchant account infrastructures through secure orchestration layers rather than replacing them outright.

Industry reports highlight that regulatory updates in multiple jurisdictions have encouraged standardized API specifications for mobile billing, reducing fragmentation that previously complicated fraud detection across borders, while merchants benefit from consolidated reporting that aggregates activity from both traditional accounts and mobile channels into unified dashboards.

Conclusion

The progression from merchant accounts to fraud-resistant mobile billing reflects incremental adoption of technologies that address specific vulnerabilities identified over decades of payment processing, with tokenization, real-time analytics, and regulatory alignment forming core components that continue to shape secure transaction environments. Data from diverse sources including government agencies and research institutions supports the observation that integrated approaches deliver measurable reductions in fraud exposure while maintaining operational efficiency for businesses handling recurring revenue streams.