API Pathways in Digital Wallets: How Tokenization Shields Merchant Accounts from Risks in Recurring Credit Card Transactions

Tokenization replaces sensitive credit card details with unique identifiers known as tokens, and this process plays a central role in digital wallet operations where recurring charges occur on a regular basis. Merchants who accept subscription payments benefit because the actual card numbers never reach their systems, which reduces exposure during data handling and storage phases.

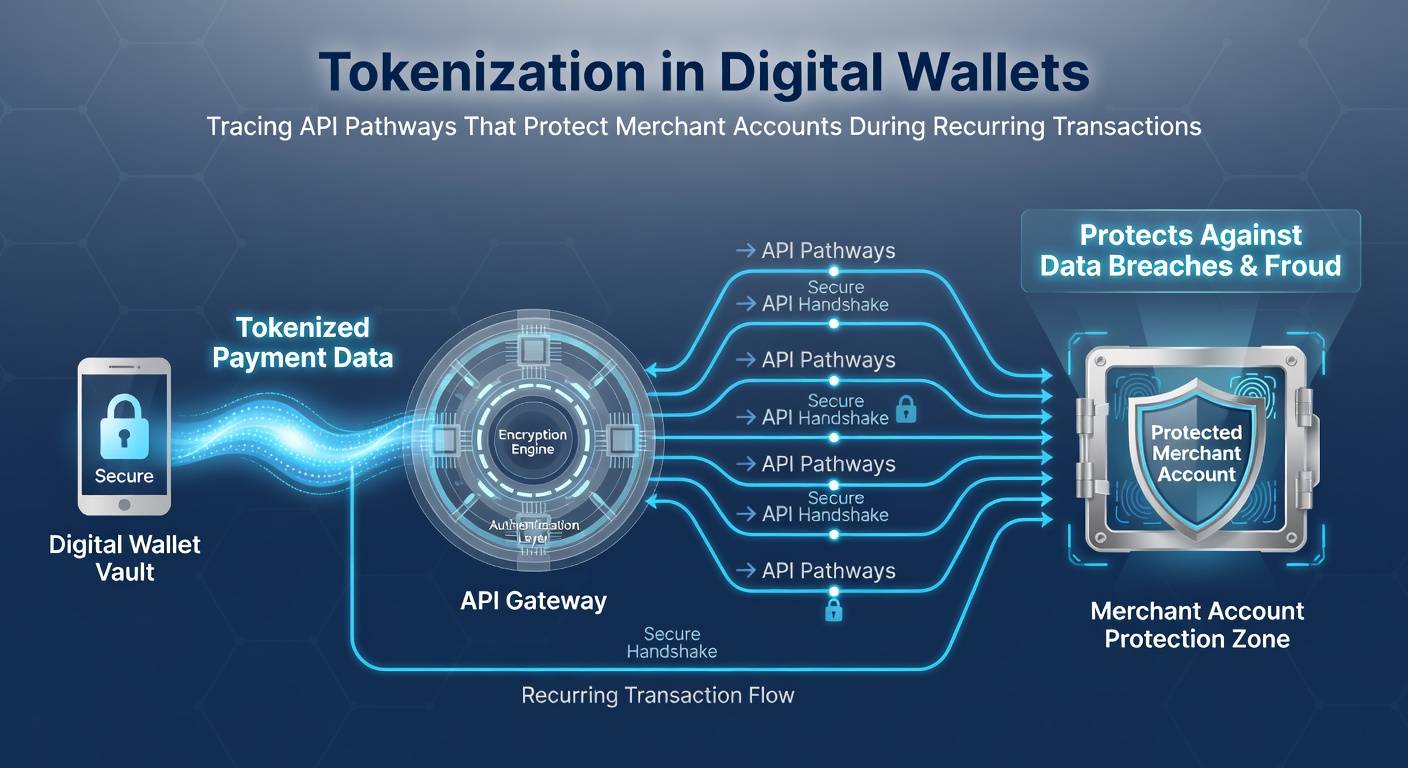

Digital wallets such as those integrated into mobile devices initiate payments by communicating with token service providers that generate and manage these tokens through secure channels. The pathways involve multiple API calls that start when a user adds a card to the wallet and continue each time a recurring transaction processes without requiring the original payment credentials to move across networks.

Understanding Token Generation and Storage Mechanisms

Card networks and issuing banks collaborate to create tokens that map back to the underlying account through a secure vault maintained by the token service provider, and this mapping allows merchants to request payments using only the token identifier. Research indicates that tokenization limits the scope of potential breaches because even if a token becomes compromised the attacker still needs additional authentication factors to access funds.

Observers note that during initial setup the wallet app sends encrypted card data to the token service provider via an API endpoint, which then validates the card with the issuer and returns a token along with domain restrictions that limit where the token can be used. Those restrictions often include specific merchant identifiers and transaction types, which helps prevent misuse in unauthorized recurring billing scenarios.

Tracing the API Sequence for Recurring Charges

When a subscription payment comes due the merchant's system initiates an API request to its payment gateway that includes the stored token rather than the card number, and the gateway forwards this request to the acquirer who routes it through the card network for authorization. The network recognizes the token and retrieves the real card details only at the final step before the issuer approves or declines the charge.

This sequence keeps merchant accounts protected because the recurring swipe never transmits full card data over the internet connection, and data shows that such limited exposure correlates with lower fraud rates in subscription-based businesses. The process repeats seamlessly each billing cycle without the customer needing to re-enter information, which maintains convenience while upholding security protocols.

Protection Layers for Merchant Accounts

Merchants gain several layers of defense through tokenization because payment credentials stay with the token service provider instead of residing in the merchant database, and this separation means that compliance with data security standards becomes simpler to achieve. According to reports from the PCI Security Standards Council, organizations that adopt tokenization for recurring transactions report fewer instances of account compromise during routine processing.

Additional safeguards come from dynamic tokens that can change with each transaction or incorporate unique cryptograms, and experts have observed that these features add friction against replay attacks where fraudsters attempt to reuse captured data. In recurring scenarios the API pathways often include checks for transaction amount consistency and billing frequency patterns, which flag anomalies before they reach the merchant account.

Integration Points Across Digital Wallet Ecosystems

Different wallet providers implement tokenization through standardized yet flexible APIs that connect to various card schemes, and this interoperability allows merchants to support multiple wallet types without maintaining separate systems for each. The pathways typically involve authentication steps where the wallet verifies user identity before releasing a token for payment use, which adds another checkpoint against unauthorized recurring charges.

Payment gateways act as intermediaries that translate between merchant platforms and the token ecosystems, handling the routing while ensuring that tokens remain valid only for approved use cases. Figures reveal steady growth in token usage for subscriptions as more businesses move toward automated billing models that rely on these secure channels.

Developments Projected Through May 2026

By May 2026 industry analyses project wider deployment of advanced token features such as network tokenization that operates independently of specific wallets, and these updates aim to further streamline recurring payments across borders while maintaining the same protective barriers for merchant accounts. Regulatory bodies in multiple regions continue to emphasize tokenization as a recommended practice for handling stored credentials in subscription services.

Those who've studied payment trends know that API enhancements scheduled for release around that period focus on real-time token lifecycle management, allowing merchants to update or revoke tokens instantly when customer subscriptions change status. Such capabilities reduce administrative overhead and keep security protocols aligned with evolving transaction patterns.

Conclusion

Tokenization combined with precise API pathways delivers measurable protection for merchant accounts during recurring credit card activity by keeping sensitive data isolated and transactions traceable at every step. Businesses that incorporate these methods see reduced risk exposure alongside reliable processing for ongoing customer relationships, and ongoing refinements in the field support continued adoption across diverse payment environments.