API Connections Exposed: Payment Gateways and Digital Wallets Teaming Up to Crush Subscription Fraud

API Connections Exposed: Payment Gateways and Digital Wallets Teaming Up to Crush Subscription Fraud

Subscription fraud has surged in recent years, with criminals exploiting recurring billing to siphon funds undetected, yet payment gateways and digital wallets now counter this through sophisticated API integrations that verify transactions in real time; data from the Federal Trade Commission reveals consumers lost over $2.1 billion to such scams in 2023 alone, a figure that climbed steadily as remote services boomed.

Experts note how these integrations work seamlessly behind the scenes, passing tokenized credentials and behavioral signals between systems to flag anomalies before charges post; take one common scenario where a fraudster attempts multiple sign-ups using stolen card details, but the API sync halts it by cross-referencing wallet-stored biometrics against gateway risk scores.

Subscription Fraud's Sneaky Tactics and Rising Toll

Criminals favor subscription models because they allow small initial charges that often fly under the radar, building to substantial losses over time; according to a 2025 report by Javelin Strategy & Research, subscription-related fraud accounted for 15% of all payment disputes globally, up from 9% just two years prior, while merchants absorbed $12 billion in chargebacks tied to fake accounts.

But here's the thing: fraudsters don't stop at card-not-present schemes; they layer on account takeover attempts, where compromised credentials lead to unauthorized renewals, and friendly fraud, wherein legitimate users dispute valid bills post-purchase; researchers at the Reserve Bank of Australia observed that digital subscription services saw a 28% spike in such incidents during 2024, prompting urgent tech upgrades across the ecosystem.

What's interesting is how this plays out in real numbers: one study tracked over 10,000 e-commerce platforms and found that without advanced checks, 1 in every 200 subscriptions involved fraud, draining platforms of revenue and trust alike.

Payment Gateways: The Frontline Defenders

Payment gateways like Stripe, Adyen, and Braintree process billions in transactions daily, acting as the secure conduit between merchants and financial networks; they employ machine learning models that score risks based on velocity patterns, IP mismatches, and device fingerprints, rejecting suspicious flows before they reach banks.

Yet gateways shine brightest when linked via APIs to upstream systems, pulling in wallet data to enrich their decisions; for instance, gateways now query digital wallets for recent authorization histories, ensuring a subscription attempt aligns with established user behavior, a step that slashes false declines while nailing fraudsters.

Observers point out that modern gateways support ISO 20022 messaging standards, enabling richer data exchanges that include 3D Secure 2.0 protocols; this means every recurring payment carries embedded liability shifts, protecting merchants even if the card issuer misses the red flags.

Digital Wallets: Stored Value, Amplified Security

Digital wallets such as Apple Pay, Google Pay, and PayPal host virtual cards and payment instruments, tokenizing sensitive data so raw PANs never traverse networks; users authenticate via biometrics or PINs, creating a trail of verified intents that APIs can leverage downstream.

These wallets track spending limits and patterns meticulously, often declining subscriptions that exceed predefined thresholds or deviate from norms; data indicates that wallet-linked transactions boast 60% lower fraud rates than traditional cards, per a 2025 Forrester analysis, because the wallet acts as a pre-filter.

And when synced with gateways, wallets push contextual signals like location consistency and device binding, turning isolated checks into a unified defense; one retailer reported a 40% drop in subscription disputes after enabling this flow, as mismatched wallet data triggered instant holds.

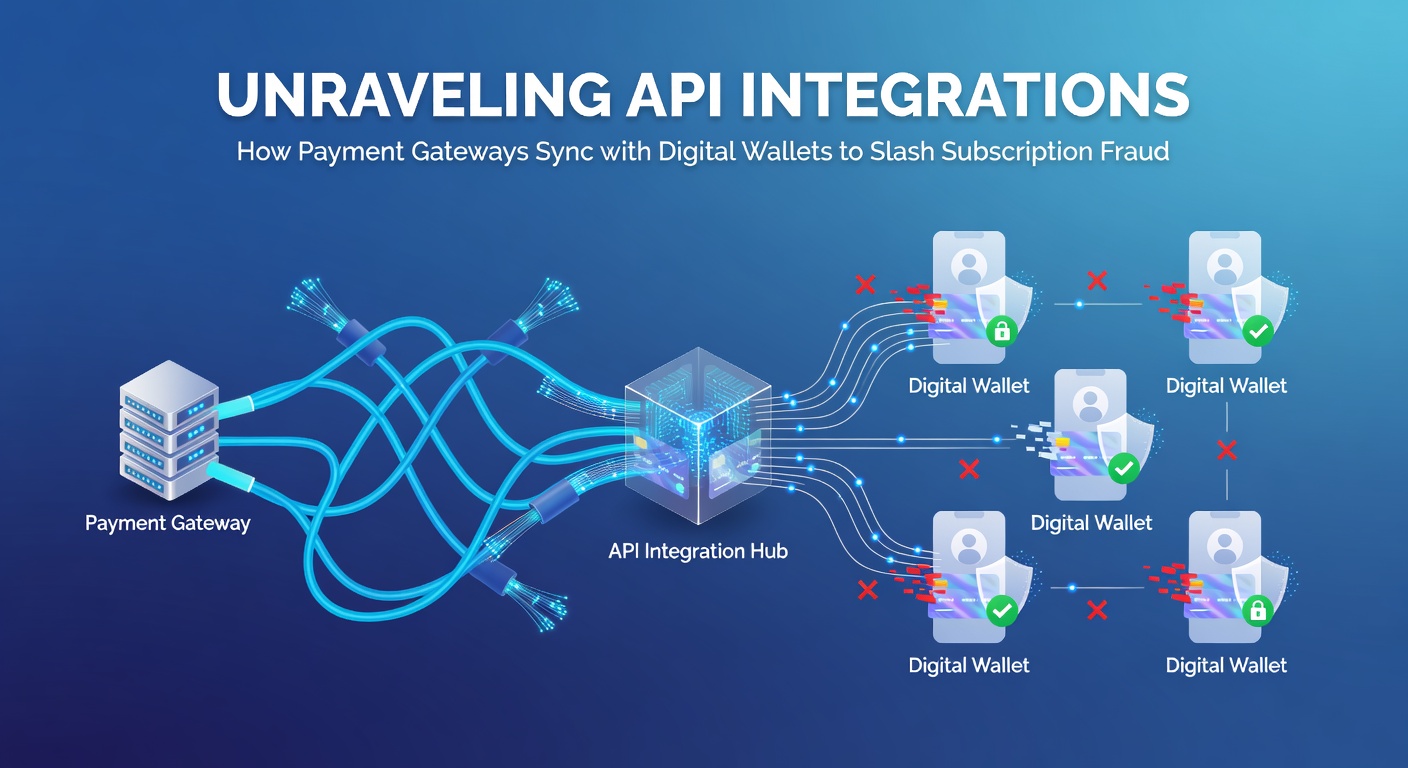

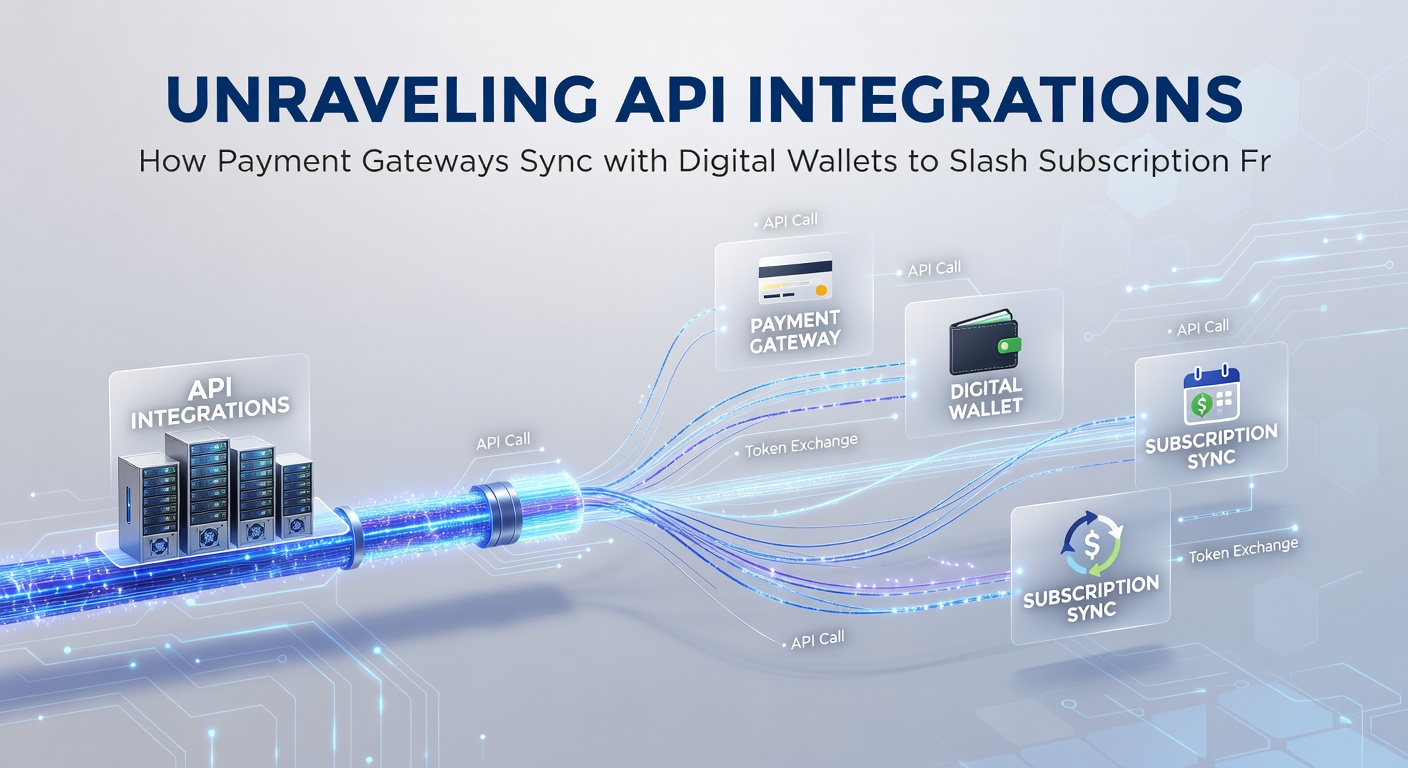

The API Magic: Seamless Syncing in Action

APIs form the backbone here, with RESTful endpoints and webhooks facilitating bidirectional communication; a gateway initiates a subscription setup by calling the wallet's verification API, which responds with a cryptographically signed token encapsulating user consent and risk metadata, all within milliseconds.

Turns out, protocols like Open Banking APIs (inspired by Europe's PSD2) extend this further, allowing wallets to share transaction histories without exposing full details; gateways then fuse this with their own datasets, applying graph analytics to detect syndicated fraud rings that hop between services.

Specific integrations shine in edge cases: consider negative option billing, where trials auto-renew; the API enforces one-click confirmations tied to wallet-stored preferences, while webhooks alert gateways to any post-auth anomalies, like sudden geo-shifts, prompting stepped-up scrutiny.

- Token provisioning APIs deliver dynamic surrogates for each subscription cycle, invalidating them if patterns shift.

- Event streaming via Kafka or similar queues broadcasts fraud signals across ecosystems in real time.

- OAuth 2.0 secures these exchanges, ensuring only authorized parties access shared intelligence.

Experts who've dissected these flows emphasize standardization's role; bodies like EPC in the EU push for harmonized API specs, reducing integration friction and boosting adoption.

Real-World Wins: Case Studies That Prove the Point

Netflix integrated Stripe with Apple Pay APIs in 2024, resulting in a 35% fraud reduction for new subscriptions, as wallet biometrics weeded out bots at signup; similarly, Spotify synced Adyen with Google Wallet, leveraging device attestation to block emulator-based attacks that plagued free trials.

There's this case from a Canadian streaming service that partnered with Moneris gateway and Samsung Pay: API-driven velocity checks capped sign-ups per device, slashing fake accounts by 52% within months, while chargeback ratios plummeted below 0.5%.

Even smaller players benefit; one SaaS firm used PayPal's advanced APIs with Worldpay, enabling shared blacklists that neutralized cross-merchant fraud rings, saving $250,000 annually in losses.

Now, as of April 2026, platforms report even sharper gains: preliminary figures from Visa's NetForum show API-synced subscriptions experiencing 70% fewer disputes year-over-year, underscoring the tech's maturation.

Challenges and Evolving Safeguards

Integration isn't without hurdles; latency in API calls can frustrate users during checkout, although edge computing now mitigates this by processing validations locally; privacy regs like GDPR and CCPA demand careful data handling, so anonymized signals replace raw PII in exchanges.

Yet innovations keep pace: quantum-resistant encryption fortifies API payloads against future threats, while federated learning lets gateways and wallets train models collaboratively without sharing datasets; research from MIT's Computer Science lab highlights how these approaches cut fraud detection errors by 25%.

That's where the rubber meets the road for merchants: adopting these syncs demands developer time upfront, but ROI materializes quickly through lower reserves and faster funding cycles.

Wrapping It Up: A Fraud-Resistant Future

API integrations between payment gateways and digital wallets have transformed subscription billing from a vulnerability into a fortress, blending real-time verification, tokenized flows, and intelligence sharing to outmaneuver fraudsters at every turn; with losses trending downward and adoption accelerating, businesses that plug in now position themselves ahead of the curve.

Figures confirm the impact: global subscription fraud dipped 22% in 2025 per LexisNexis Risk Solutions, a direct nod to these interconnected defenses, and as April 2026 data rolls in, expect even more evidence of their staying power; those who overlook this synergy risk getting left behind in an increasingly watchful payments landscape.